A senior White House official has accused major banking trade leaders of refusing to join earlier talks on stablecoin rewards, escalating a dispute that has become one of the final pressure points ahead of the Senate Banking Committee taking up the CLARITY Act this week.

In a May 11 post on the social media platform X, Patrick Witt, executive director of the White House Presidential Advisory Committee on Digital Assets, said he had asked American Bankers Association President Rob Nichols and other bank trade CEOs to attend the February meetings aimed at resolving the question of stablecoin rewards and yield.

He stated:

“I specifically requested the attendance of Mr. Nichols and other bank trade CEOs at the meetings we hosted back in February to resolve the stablecoin rewards/yield issue. They refused. I guess the White House was beneath them?”

The criticism injected the White House more directly into a fight that has divided banks, crypto companies, and lawmakers ahead of a scheduled May 14 markup of the CLARITY Act.

The bill is designed to create a broader market structure framework for digital assets, but the treatment of stablecoin rewards has become a flashpoint over competition for deposits, consumer yield, and the future shape of dollar-based payments.

Witt’s comments also reframed the timing of the banking industry’s objections. Rather than a new technical concern emerging before a committee vote, the White House official cast the dispute as an unresolved issue that banking leaders had an opportunity to address months earlier.

Banks reopen stablecoin rewards fight before markup

Over the weekend, the American Bankers Association (ABA) urged bank executives and employees to press senators for tighter restrictions in the CLARITY Act before the committee vote, warning that the current bill could still allow crypto firms to offer reward structures that resemble interest on deposit-like products.

Nichols told bankers that lawmakers needed to hear from the industry before the legislation advanced.

The ABA’s concern is that stablecoin issuers, exchanges, or related companies could attract customer funds by offering returns on assets that compete directly with traditional bank deposits.

That argument has become central to the US bank lobby’s campaign.

Banks rely on deposits as a funding base for loans to households, small businesses, farms, and corporations. If customers move cash into stablecoins that offer rewards, banks argue that lenders could face higher funding costs, tighter margins, and less capacity to extend credit.

The banking industry has described the current compromise language as leaving a loophole.

In its view, a ban on stablecoin issuers paying yield would be insufficient if affiliated exchanges, brokers, or other crypto platforms could deliver similar economic benefits through rewards, rebates, or incentive programs.

That position has put banks at odds with crypto companies that see the rewards language as a basic competition issue.

Stablecoin reserves are typically held in cash, short-term Treasuries, or other liquid instruments that generate income. The policy fight centers on whether consumers should be able to receive part of that return, and which type of institution should be allowed to offer it.

The recent Senate compromise has attempted to separate passive yield from activity-based rewards.

That distinction was meant to prevent stablecoins from becoming direct substitutes for interest-bearing deposits while preserving room for crypto platforms to reward users for participation, payments, or other services.

White House analysis undercuts the lending warning

The banking industry’s warnings have met resistance from the White House’s own economic analysis.

The Council of Economic Advisers said in an April report that banning stablecoin yield would provide only a marginal lift to bank lending under its baseline assumptions. The CEA estimated that such a ban would increase bank lending by about $2.1 billion, equal to roughly 0.02% of total lending in the base case.

That finding gives the administration a counterweight to the banking sector’s claim that stablecoin rewards could meaningfully damage credit creation.

The report argued that most stablecoin reserves would not be permanently removed from the banking system. Instead, reserves held in cash, bank deposits, or Treasury instruments would continue to circulate through financial markets in different forms.

The CEA also said a more severe impact would require a much larger stablecoin market and more restrictive assumptions about how reserves are held. In the administration’s framing, stablecoin rewards may affect bank margins, but the baseline effect on lending capacity appears limited.

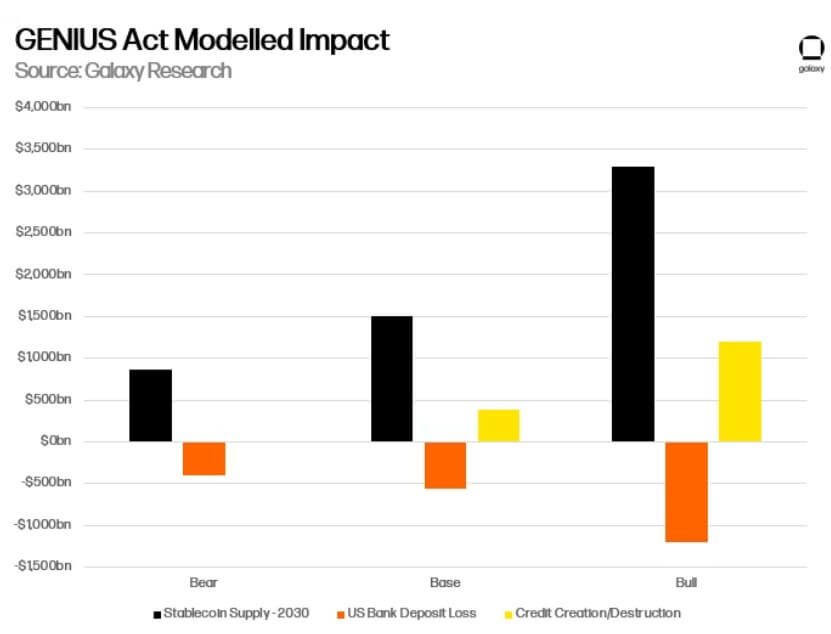

Moreover, a separate analysis by Galaxy Research furthered the argument by focusing on the international flow of dollars.

Galaxy said banks were overstating the risk that stablecoin growth would simply drain domestic deposits. Its model projected that much of the growth under a regulated stablecoin framework would come from offshore users seeking easier access to dollar-denominated assets.

That finding changes the economic lens. If stablecoins mostly draw funds from US bank accounts, banks face a direct deposit migration problem.

However, if much of the growth comes from foreign users moving into dollar stablecoins, the effect could be an inflow into US financial infrastructure rather than a one-way drain from domestic lenders.

Galaxy estimated that 60% to 70% of stablecoin growth under the GENIUS Act framework could originate offshore. It also projected that imported deposits from foreign demand could exceed domestic deposit migration by roughly 2:1.

The firm said each newly minted stablecoin dollar could generate about 32 cents of net US credit, with total credit expansion reaching about $400 billion through 2030 in its base case and as much as $1.2 trillion in a stronger growth scenario.

It also projected that stablecoin reserve demand could compress Treasury bill yields by 3 to 5 basis points, potentially lowering federal borrowing costs.

Meanwhile, Galaxy did not dismiss the pressure on banks. The report said some low-cost deposits would likely migrate, funding costs could rise at the margin, and net interest margins could compress in business lines sensitive to rate competition.

Still, the firm concluded that stablecoins could pressure banks that rely on cheap deposits, increase demand for US Treasury bills, import offshore dollar capital, and expand the reach of the US financial system.

Crypto allies accuse banks of protecting margins

Crypto advocacy groups have seized on the ABA’s push as evidence that banks are trying to block competition days before the committee vote on the CLARITY Act.

Coinbase-backed Stand With Crypto urged supporters to contact senators, saying banking lobbyists were trying to weaken stablecoin rewards language before the markup.

The group framed the dispute as a consumer-rights issue, arguing that users should be able to earn returns on their own digital assets rather than have that value captured by intermediaries.

Cody Carbone, CEO of The Digital Chamber, said banks had months to negotiate over the issue and were now trying to force changes late in the process. He described the ABA campaign as an attempt to shield incumbents from competition after earlier opportunities to engage had passed.

Sen. Bernie Moreno, an Ohio Republican on the Banking Committee and a supporter of crypto legislation, used sharper language about the bank’s opposition to CLARITY Act.

He accused the “banking cartel” of trying to preserve a system in which banks pay depositors little while earning profits from lending and securities portfolios.

Moreno wrote on X:

“During the Biden era, these same banks worked hand-in-glove with Sen. Warren and her allies to debank Americans, including President Trump’s own family. They shut down accounts of conservatives, patriots, and anyone who dared challenge the regime, all while regulators applied pressure under schemes like Operation Choke Point 2.0. It wasn’t about risk. It was about political control. Now that innovative stablecoins threaten to break their monopoly and give you actual financial freedom? They’re running to Congress again, screaming about ‘threats to economic growth and financial stability.’”

Moreno’s statement showed how the stablecoin rewards dispute has moved beyond technical drafting.

The fight now carries a broader political message about financial competition, consumer returns, and resentment toward large banking institutions.

That rhetoric could help crypto advocates rally support, especially among Republicans who view stablecoins as part of a broader agenda around financial innovation and dollar competitiveness.

However, it also risks hardening opposition from lawmakers who are already concerned that crypto firms are seeking bank-like privileges without equivalent oversight.

Markup will test whether the stablecoin compromise can hold

The Senate Banking Committee’s May 14 markup will show whether the rewards compromise can withstand a coordinated pushback from the banking industry.

If the committee advances the CLARITY Act with the current language largely intact, crypto firms will claim momentum, and banks will likely shift their campaign to the full Senate.

If lawmakers tighten the rewards provisions, the banking industry will have succeeded in reopening one of the most contested parts of the bill at the final stage before markup.

Meanwhile, the vote will also test the broader coalition behind the CLARITY Act. Republicans have pushed digital-asset legislation as a priority, while some Democrats have remained open to a market-structure bill if it includes stronger consumer protections, ethics, and anti-money-laundering provisions.

The stablecoin fight complicates that effort because it cuts across several policy lines at once. It raises questions about bank funding, consumer yield, Treasury demand, offshore dollar usage, and the role of crypto firms in payments.

That gives senators several reasons to demand changes, but also makes the issue difficult to settle cleanly.

Bitcoin

Bitcoin  Ethereum

Ethereum  Tether

Tether  BNB

BNB  USDC

USDC  XRP

XRP  Solana

Solana  TRON

TRON  Figure Heloc

Figure Heloc {kind=link}