BlackRock’s 1% to 2% Bitcoin allocation range reads as a bullish nod to advisor adoption, but it also works as a boundary. Once Bitcoin is included in a model portfolio, its upside runs through rebalancing bands, tax location, and sometimes a loan that keeps the position intact.

BlackRock Investment Institute frames 1% to 2% as a reasonable multi-asset range, provided the investor believes in continued adoption and can stomach sharp drops.

The firm sizes the position based on its contribution to overall portfolio risk, and that risk climbs quickly in a standard 60/40 mix. A 1% Bitcoin allocation adds roughly 2% to total portfolio risk, a 2% allocation adds roughly 5%, and a 4% allocation adds roughly 14%.

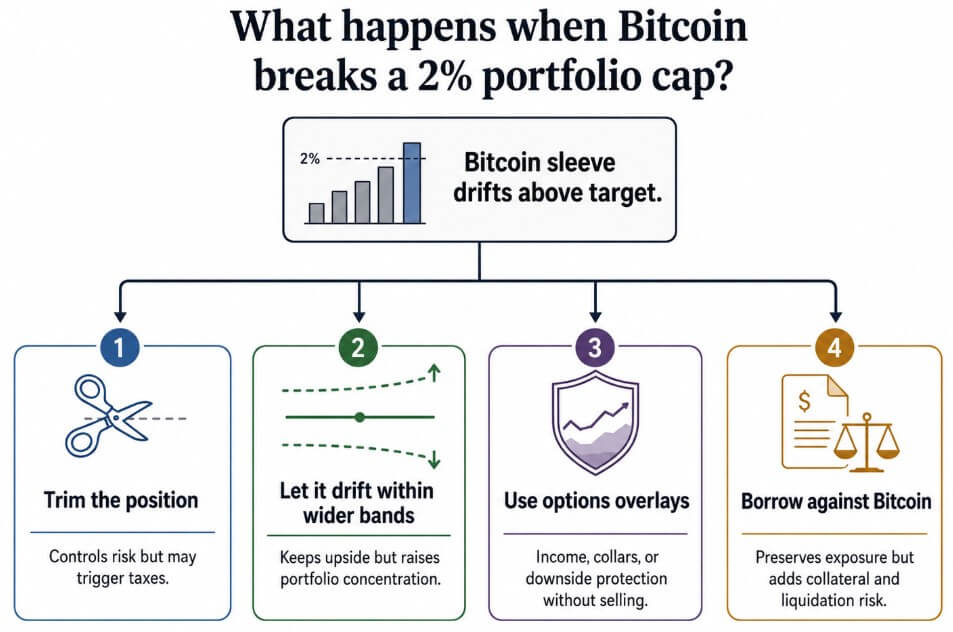

That risk math turns the ceiling into a live decision point. If Bitcoin outruns stocks and bonds within the model, an advisor can trim it, let it drift, hedge it, or move exposure elsewhere.

A 2% Bitcoin sleeve needs roughly a 51.5% gain, with the rest of the portfolio flat, to drift to 3%. It needs roughly a 104% gain to drift to 4%, the point at which resetting the position to 2% would mean selling almost half the sleeve.

| BTC allocation / drift point | Portfolio impact | What it forces advisors to decide |

|---|---|---|

| 1% BTC allocation | ~2% of total portfolio risk | Small enough to fit inside a traditional risk budget |

| 2% BTC allocation | ~5% of total portfolio risk | BlackRock’s upper range; becomes the key management ceiling |

| 4% BTC allocation | ~14% of total portfolio risk | Bitcoin starts dominating risk contribution |

| 2% sleeve after ~51.5% BTC rally | Drifts to ~3% | Advisor must decide whether to trim, hedge, or let it run |

| 2% sleeve after ~104% BTC rally | Drifts to ~4% | Resetting to 2% means selling about half the BTC sleeve |

BlackRock’s IBIT alone had nearly $60 billion in net flows as of July 2, a size at which portfolio management choices start to matter for the wider market.

Citi cut its 12-month Bitcoin price target to $82,000 from $112,000 on July 1 and dropped its inflow assumption to zero from $10 billion.

The firm pointed to Bitcoin ETF flows running negative year-to-date, and Farside Investors’ data showed that US-traded spot Bitcoin ETFs lost over $2.7 billion across 10 trading days from late June to July 1.

Why selling hurts

For a long-time Bitcoin holder, selling to stay under a cap can feel like giving up the wrong asset.

Mauricio Di Bartolomeo, co-founder and chief strategy officer of the Bitcoin lending firm Ledn, sees a wide range of borrowers.

They include public and private companies operating on a Bitcoin standard, as well as households in Latin America running circular economies. Couples also borrow against Bitcoin to buy their first home.

He told CryptoSlate that “borrowers come in all shapes and sizes,” and what connects them is a preference for financing over a sale, keeping the asset they consider their strongest holding.

Taxes play a part in that decision, but Di Bartolomeo says the math holds up on its own, taxes aside. He points to a borrower who took a Bitcoin-backed loan in January 2020 and managed it responsibly.

Even net of interest and fees, that person would sit in a stronger financial position today than someone who sold Bitcoin outright that same month.

Di Bartolomeo estimated that borrowers using Bitcoin as collateral should set aside at least 100% of that collateral’s value to handle market volatility. Once someone borrows against over half of a Bitcoin portfolio, the cushion protecting them from a sharp drawdown gets thin.

The case against forced selling

Kelly Ye, co-founder and chief investment officer of CoinBridge, pushed back on the assumption that model portfolios already drive Bitcoin ETF flows.

She pointed to Morgan Stanley’s figures, noting that roughly 80% of Bitcoin ETF activity on the firm’s platform remains self-directed, with about 20% routed through advisors.

Large wirehouses typically require six to twelve months of performance history, operational due diligence, and compliance review. She said that only then does a new ETF earn a spot in a centralized model.

That timeline keeps most of today’s Bitcoin exposure in the hands of individual investors making their own decisions.

Even once advisors adopt Bitcoin, Ye expects a broader toolkit to handle most of the work, with a sale as a last resort. Rebalancing bands can be set wider for a volatile asset than for bonds or large-cap stocks.

Advisors can rebalance using new client contributions, trim only a portion of a position, or place the Bitcoin sleeve in an IRA or a Roth account. A sale inside one of those accounts avoids an immediate tax bill.

Many current ETF holders are still near their entry price, Ye notes. Glassnode puts the average ETF holder’s cost basis near $83,000, well above Bitcoin’s price through the back half of the second quarter.

That means a large share of holders would show a loss if they sold today.

The options market backs her up, as IBIT options volume now rivals native Bitcoin options markets.

OCC reported 689.5 million ETF options contracts traded in June, up 69.7% from a year earlier. Kaiko and MerQube data cited by ETF Express show IBIT options open interest peaked at $53.3 billion in its first year.

Goldman Sachs has filed for a Bitcoin ETF built to pair Bitcoin exposure with income from options trades, joining a set of tools built almost entirely since the ETF’s 2024 launch.

Letting the winner run

If the toolkit does the work, Bitcoin’s rally keeps compounding within advisors’ books, and sales stay occasional. Wider tolerance bands absorb the early drift, and new client cash flows nudge portfolios back toward target on their own.

Retirement accounts hold a larger share of the Bitcoin sleeve over time, reducing the tax bill at each rebalance.

Options overlays cover the rest, letting advisors collect income or buy protection while keeping the underlying position intact. In this version, Wall Street financializes Bitcoin, and the position continues to compound.

Trimming on schedule

The alternative path runs through tighter mechanics. If large platforms build Bitcoin into models using the same narrow bands they apply to stocks and bonds, a rally triggers a trim fast.

Bitwise says assets tracking third-party model portfolios grew from $400 billion in 2023 to over $645 billion in 2025, a 62% jump.

As the model-portfolio infrastructure grows, a 2% Bitcoin sleeve becomes a recurring source of supply whenever Bitcoin rallies hard, and a winning position becomes a scheduled sale.

If Bitcoin-backed borrowing grows at the same pace with less discipline, a sharp drawdown could add forced liquidations on top of the trims.

| Scenario | What happens | Market implication |

|---|---|---|

| Managed drift | Advisors allow Bitcoin to move above 2% inside wider tolerance bands | Limited forced selling; Bitcoin compounds inside portfolios |

| Tax-aware adoption | More BTC ETF exposure moves into IRAs, Roth accounts, and retirement plans | Rebalancing becomes less tax-sensitive |

| Options-led management | Advisors use covered calls, collars, or downside puts instead of selling spot exposure | Volatility is managed without fully reducing BTC exposure |

| Mechanical trimming | Model portfolios apply narrow bands and sell once BTC runs above target | Bitcoin rallies create recurring supply from advisors |

| Collateral stress | Borrowers overuse Bitcoin-backed loans and BTC sells off sharply | Liquidations amplify downside rather than avoiding sales |

Bitcoin is the asset that was once defined by hold-forever conviction and is now becoming a managed sleeve, with rules for rebalancing, tax location, and when a loan replaces a sale.

Management is the open fight that runs through rebalancing bands, tax location, and, for some holders, a loan that keeps the Bitcoin where it is.

Bitcoin

Bitcoin  Ethereum

Ethereum  Tether

Tether  BNB

BNB  USDC

USDC  XRP

XRP  Solana

Solana  TRON

TRON  Figure Heloc

Figure Heloc  Hyperliquid

Hyperliquid {kind=link}