A nearly $150 million prediction market has devolved into chaos after the platform Polymarket moved to deny payouts to traders who accurately predicted that corporate treasury firm Strategy would sell a portion of its Bitcoin holdings.

The dispute centers on a fundamental disconnect between when an event occurs and when it is publicly disclosed, exposing structural flaws in how decentralized prediction markets resolve multibillion-dollar wagers. Bettors are now locked in a bitter dispute over a technicality that could wipe out millions of dollars in payouts traders believed were guaranteed.

On June 1, Strategy, the business intelligence firm formerly known as MicroStrategy, which holds nearly $60 billion of the top crypto asset, filed a regulatory document confirming it sold 32 Bitcoin, valued at roughly $2.5 million, between May 26 and May 31.

For participants in a Polymarket contract asking whether Strategy would sell any of its Bitcoin by May 31, the 8-K filing appeared to be definitive proof of a “Yes” outcome.

However, the market is currently navigating a contested resolution process that heavily favors “No.”

Polymarket administrators issued a post-deadline clarification stating that, because the public confirmation of the sale did not emerge until June 1, the transaction does not qualify under the platform’s operational customs.

The situation has sparked widespread allegations of market manipulation, drawing intense scrutiny to the mechanics of decentralized betting at a time when prediction platforms are striving for mainstream financial legitimacy.

The timeline of the contested Polymarket trade

The ongoing controversy stems from the contract’s specific wording, which stated that the market would resolve to “Yes” if Strategy sold any of its Bitcoin by 11:59 p.m. ET on May 31.

The rules explicitly designated the company’s public disclosures and on-chain data as the primary sources of resolution.

When Strategy filed its mandatory 8-K disclosure on June 1, the market remained open for active trading. Observing that the firm had executed a sale objectively before the May 31 deadline, several traders rushed to capitalize on what they perceived as a pricing inefficiency.

One market participant, operating under the pseudonym willo2, staked $527,000 on “Yes” after reading the regulatory filing. Because the market was pricing the odds of a sale at around 80 cents on the dollar even after the disclosure, the trader anticipated a 20% arbitrage opportunity.

Instead, the trader lost the entire half-million-dollar principal. Following the influx of capital, Polymarket added a clarification to the market description, stating that confirmations outside the specified timeframe would not be honored.

Speaking on these events, Willo wrote on X:

“This was straight-up NOT part of the rules. It was not written down on the market, it did not make sense – and most of all, Polymarket didn’t even believe it themselves. Why? Because if it was true, the market would have closed on May 31st. The market didn’t close.”

Market analysts have widely condemned the sequence of events. Jeff Dorman, chief investment officer at the digital asset management firm Arca, pointed out a critical logical inconsistency in the platform’s handling of the timeline.

Dorman noted that if the contract’s strict parameters dictated an end precisely at midnight on May 31, the platform should have halted all trading at that exact moment.

According to him, allowing participants to continue buying shares on June 1 while retroactively enforcing a May 31 confirmation deadline created a trap for traders relying on traditional legal interpretations of the contract text.

Jonatan Pallesen, a data scientist who monitors decentralized platforms, characterized the platform’s behavior as a form of fraud by omission.

Pallesen argued that while requiring news confirmation to align with the event deadline is a reasonable safeguard against indefinite market delays, failing to explicitly codify that custom in the contract rules exploits retail bettors.

Institutional traders familiar with the platform’s unspoken conventions were able to extract significant capital from users who reasonably assumed that a completed sale meant a winning ticket.

The UMA oracle vulnerability

The Strategy dispute has escalated from a single contract into a referendum on Polymarket’s underlying settlement architecture.

Unlike traditional financial exchanges that rely on centralized clearinghouses and legal compliance departments to settle derivatives, Polymarket outsources its truth-finding to Universal Market Access (UMA).

UMA operates as an “optimistic oracle,” a decentralized network where token holders vote to resolve disputed outcomes.

Under this framework, any user can challenge a proposed market settlement by staking a $750 bond. If the outcome is contested multiple times, the decision defaults to a vote by UMA cryptocurrency holders.

The ultimate payout is determined by the weight of tokens cast, rather than an objective judicial review of the facts.

Critics argue that this system is highly vulnerable to manipulation. Eric Conner, a prominent cryptocurrency analyst, noted that the token-voting model is structurally compromised.

Conner argued that large token holders, often referred to as whales, can weaponize ambiguous contract rules to protect their own financial positions and override objective reality to prevent massive losses.

Recent data support these concerns. A WSJ investigation into the platform’s voting mechanics revealed that the ten largest wallets account for more than half of the votes in most Polymarket disputes.

Furthermore, roughly 60% of active UMA voters were directly linked to live Polymarket accounts, and one in five contested markets featured voters who held a direct financial stake in the outcome they were adjudicating.

Polymarket has already recorded over 1,150 disputed markets in the first five months of 2026, eclipsing its entire total for the previous year.

The platform itself has limited recourse, as its decentralized structure technically prevents internal management from overriding a finalized UMA token vote.

Mainstream growth meets decentralized friction

The timing of the $150 million dispute is precarious for the prediction market sector, which has aggressively expanded its footprint into traditional finance and media over the past few years.

During this period, the platforms Polymarket and Kalshi have actively distanced themselves from being labeled as unregulated crypto casinos.

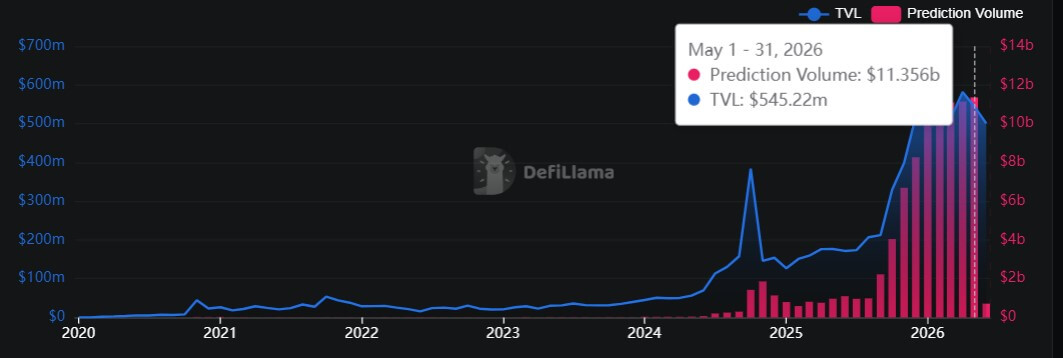

However, they have seen their trading volume increase rapidly to exceed $10 billion in May 2026. This marks a tenfold increase from the same period last year, per DeFiLlama data.

At the same time, they have established content and data integration agreements with major institutions, including the New York Stock Exchange, Dow Jones, The Associated Press, and Fox News.

This rapid institutionalization follows years of intense regulatory friction. In 2022, the Commodity Futures Trading Commission (CFTC) forced Polymarket to shut down its US operations and relocate abroad.

Kalshi subsequently engaged in a prolonged legal battle with the CFTC over the right to host political event contracts, ultimately winning a landmark federal court case in late 2024.

However, the regulatory environment shifted after the 2024 presidential election, which the platforms correctly predicted would be a Donald Trump victory.

Since then, the platforms have enjoyed significant regulatory backing, with Polymarket acquiring a federally licensed derivatives exchange, and the CFTC also asserting its exclusive right to regulate these markets.

CFTC Chairman Michael S. Selig said:

“Event contracts allow businesses and individuals to hedge event-driven risks, enable investors to manage portfolio exposure, and provide the public with information about the outcome of future events. These products are commodity derivatives and squarely within the CFTC’s regulatory remit.

Despite securing regulatory footholds, the fundamental mechanics of decentralized prediction markets remain highly experimental.

In traditional equity markets, deep liquidity and strict regulatory oversight generally ensure that asset prices reflect material reality.

On platforms governed by tokenized voting systems, the definition of reality is still up for debate.

Until these structural dispute mechanisms mature, traders navigating the booming prediction market economy remain at the mercy of unwritten rules and decentralized juries.

Bitcoin

Bitcoin  Ethereum

Ethereum  Tether

Tether  BNB

BNB  USDC

USDC  XRP

XRP  Solana

Solana  TRON

TRON  Figure Heloc

Figure Heloc  Hyperliquid

Hyperliquid {kind=link}