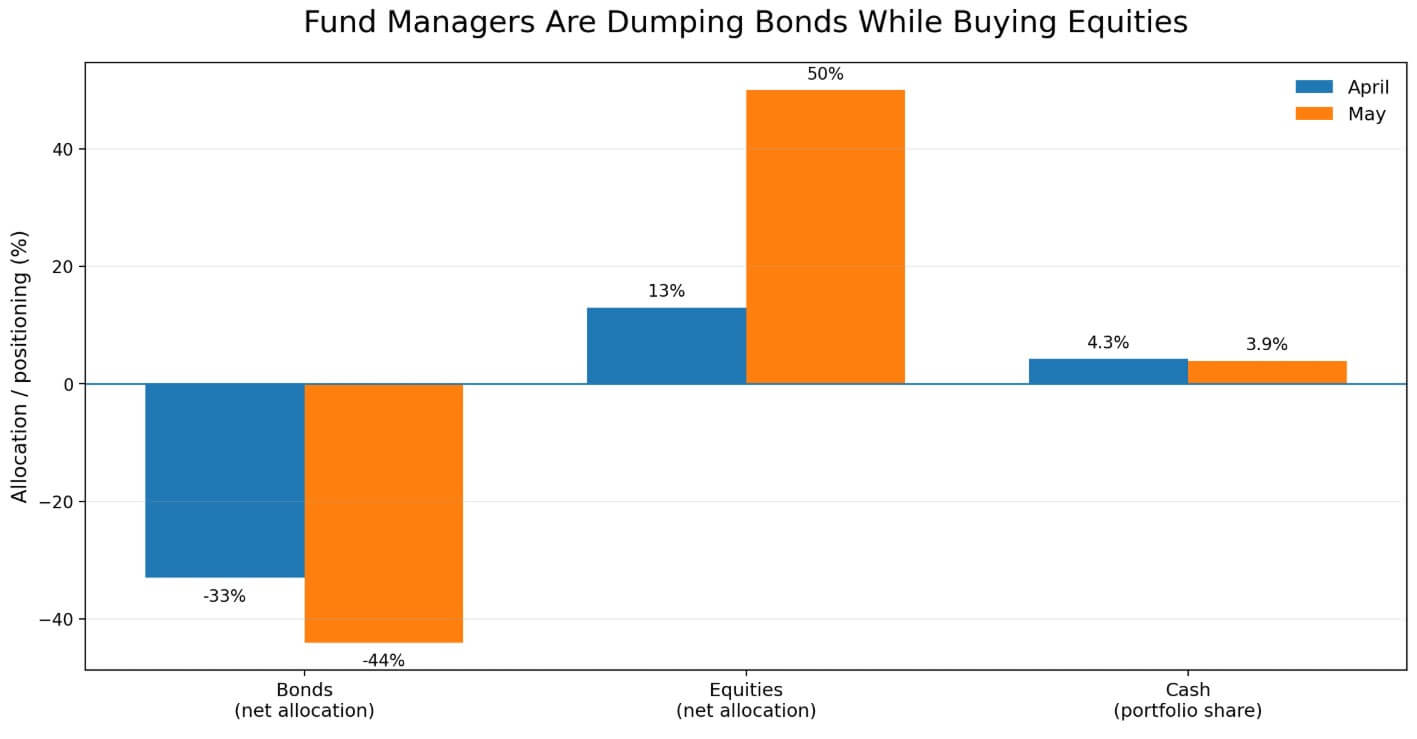

Bitcoin ETF outflows are turning rising Treasury yields into a direct test for BTC price after Bank of America’s May Global Fund Manager Survey showed professional investors cut bond allocation to a net 44% underweight, the deepest positioning since June 2022, down from 33% underweight in April.

At the same time, managers pushed global equity exposure to a net 50% overweight from 13% in April, while cash fell to 3.9% from 4.3%. Fund managers are rotating into risk while rejecting duration, doing so at the fastest pace in nearly four years.

For Bitcoin, that combination creates a problem the asset cannot ignore, as 40% of surveyed managers named second-wave inflation as the biggest tail risk, and 18% named a disorderly rise in bond yields.

The US 10-year yield hit 4.6653% on May 19, its highest level since January 2025, while the 30-year reached 5.14% and the 10-year real yield climbed to 2.13%. Real-yield repricing raises the hurdle rate for every non-yielding asset, and Bitcoin yields nothing.

The anti-duration trade is now crowded

At net 44% underweight, the anti-bond position has become the dominant consensus trade in BofA’s survey over recent history, making the next move in Treasury markets disproportionately important for risk assets.

When yields climb, duration gets repriced, borrowing conditions tighten, and capital either seeks safety or exits risk. As a 24/7 liquid asset with no contractual cash flows, Bitcoin tends to absorb that selling before less-liquid positions are cut.

That explains why Bitcoin is trading around $77,000, near the $75,000-$78,000 support area that has absorbed macro-driven selling several times this cycle.

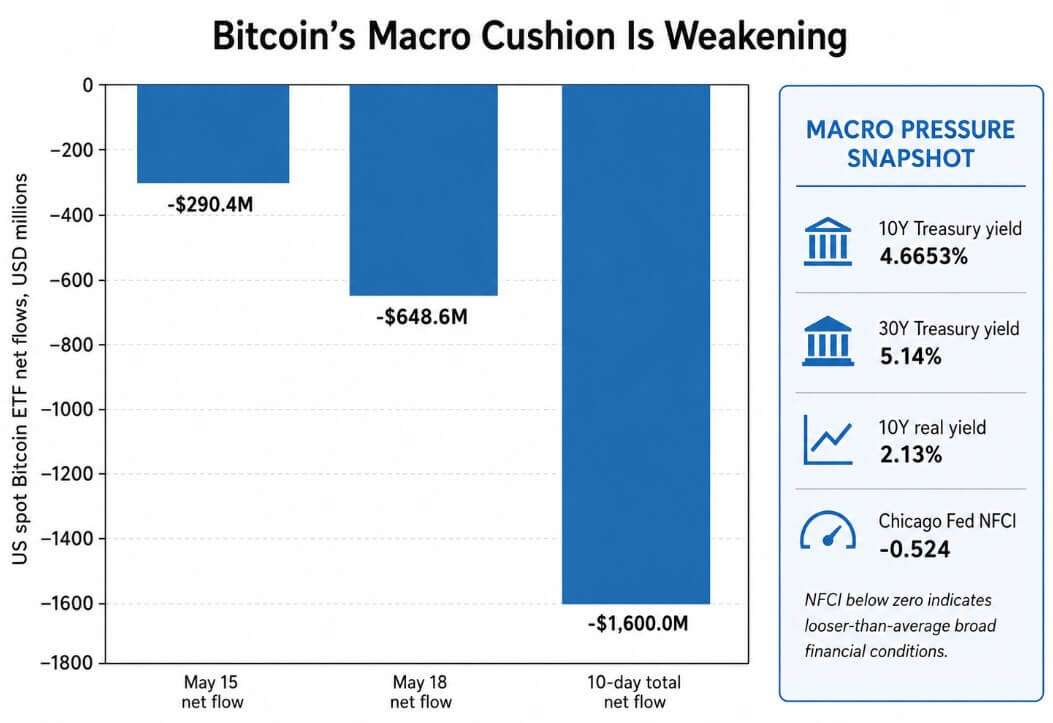

Spot Bitcoin ETFs were supposed to insulate BTC from these macro currents by anchoring institutional demand. Farside Investors’ data shows that US spot Bitcoin ETFs recorded net outflows of $648.6 million on May 18, adding to the $290.4 million of outflows registered on May 15.

Those Bitcoin ETF outflows left the 10-day total at negative $1.6 billion. The institutional bid exists, but it cannot neutralize a yield shock in real time.

The Chicago Fed’s National Financial Conditions Index sat at -0.524 for the week ending May 8, placing overall financial conditions looser than the historical average.

The Treasury market is tightening the marginal conditions for risk assets like Bitcoin, while the broader system holds well above stress thresholds.

Hedge or casualty

Long-term, Bitcoin benefits from narratives that frame government debt as structurally unsound, with a fixed supply, no central issuer, and no maturity schedule to roll.

The IMF’s April 2026 Global Financial Stability Report flagged Middle East conflict, inflation, and rollover risk in core sovereign markets as threats to global financial stability.

The OECD’s 2026 Global Debt Report noted that more price-sensitive investors now hold a larger share of government bonds as central banks step back, with foreign investors controlling 28% of global government bond holdings and hedge funds becoming more important marginal buyers in some core markets.

The Bank of Canada framed the same situation as a term-premium problem, with long-term yields staying elevated because investors demand higher compensation to absorb large debt issuance.

Together, those structural forces build a long-term case for Bitcoin as a sovereign-debt hedge.

In the short run, a disorderly spike in yields puts Bitcoin in the casualty column. When Treasury markets move fast, investors cut the most liquid positions first, and Bitcoin sits at the top of that list.

Two potential paths

If inflation data surprises to the downside or Fed rate-hike pricing fades, the anti-duration trade could reverse quickly.

A consensus net 44% underweight position in bonds carries its own fragility, as a single inflation miss could trigger a sharp unwind. Should the 10-year yield fall toward 4.20%-4.40% and the 30-year move back below 5%, financial conditions for risk assets ease.

ETF inflows would restart, the $80,000-$82,000 resistance zone would break, and Citi’s base-case 12-month Bitcoin forecast of $112,000 comes back into view, with the bank’s bull case at $165,000 anchored to stronger end-investor demand.

Lower real yields reduce the opportunity cost of holding a non-yielding asset, loosen borrowing conditions for levered buyers, and restore risk appetite. Bitcoin has historically recaptured ground quickly when those three conditions align.

The crowded anti-bond trade amplifies the potential reversal, since every fund manager who unwinds an underweight bond position also eases the macro headwind that has been suppressing BTC.

| Scenario | Treasury trigger | Market mechanism | ETF-flow implication | Bitcoin level to watch | BTC implication |

|---|---|---|---|---|---|

| Yield relief / bull path | 10Y yield falls toward 4.20%–4.40%; 30Y slips back below 5% | Anti-duration trade unwinds; real yields fall; liquidity conditions ease for non-yielding assets | Spot BTC ETF inflows restart as macro pressure fades | BTC breaks $80,000–$82,000 resistance | Citi’s $112,000 base case comes back into view; bull case near $165,000 if end-investor demand strengthens |

| Yield spike / bear path | 10Y yield breaks above 4.73%; 10Y real yield rises above 2.13%; 30Y extends above 5.14% | Duration selloff tightens marginal financial conditions; investors cut liquid risk first | ETF outflows accelerate and leveraged longs face pressure | BTC loses $75,000–$78,000 support | BTC trades as a liquidity casualty; Citi’s recessionary downside near $58,000 becomes the key risk anchor |

If the 10-year yield breaks through the technical level near 4.73% and continues higher, driven by sticky inflation, weak Treasury auctions, or geopolitical escalation, Bitcoin’s position near $75,000-$78,000 support becomes untenable.

Real yields above 2.13% make it difficult to justify the opportunity cost of holding Bitcoin relative to a government bond with a sovereign guarantee and a yield competitive with historical equity risk premia.

ETF outflows would accelerate, leveraged long positions would face margin calls, and BTC would trade as the most liquid risk asset in a deleveraging cycle.

Citi’s recessionary macro downside for Bitcoin sits at $58,000, and getting there from current levels requires a disorderly yield environment that forces simultaneous deleveraging across multiple asset classes.

The 18% of fund managers from BofA’s survey already cite a disorderly rise in yields as the biggest tail risk, and the 30-year yield at 5.14% sits close to levels that have historically triggered broader financial market volatility.

What Bitcoin ETF outflows actually signal

Bitcoin macro risk now depends on the pace at which the Treasury market tightens financial conditions relative to what ETF demand and risk appetite can absorb.

The BofA survey shows institutions rotating into equities while keeping cash lean and shedding duration. That rotation leaves Bitcoin exposed to the same yield dynamics that compress every other non-yielding asset and adds the vulnerability of operating in a 24/7, liquid market where macro sellers can exit at any hour.

If yields peak and the trade unwinds, the reversal could be fast, and the recovery from current support levels could be large.

Until Treasury yields stabilize, Bitcoin ETF outflows leave BTC on the wrong side of the most consensus macro trade in four years.

Bitcoin

Bitcoin  Ethereum

Ethereum  Tether

Tether  BNB

BNB  USDC

USDC  XRP

XRP  Solana

Solana  TRON

TRON  Figure Heloc

Figure Heloc  Hyperliquid

Hyperliquid {kind=link}