Circle’s biggest selling point may be becoming its biggest liability. On-chain investigator ZachXBT’s “Circle Files” allege that the USDC issuer has inconsistently applied its freeze powers.

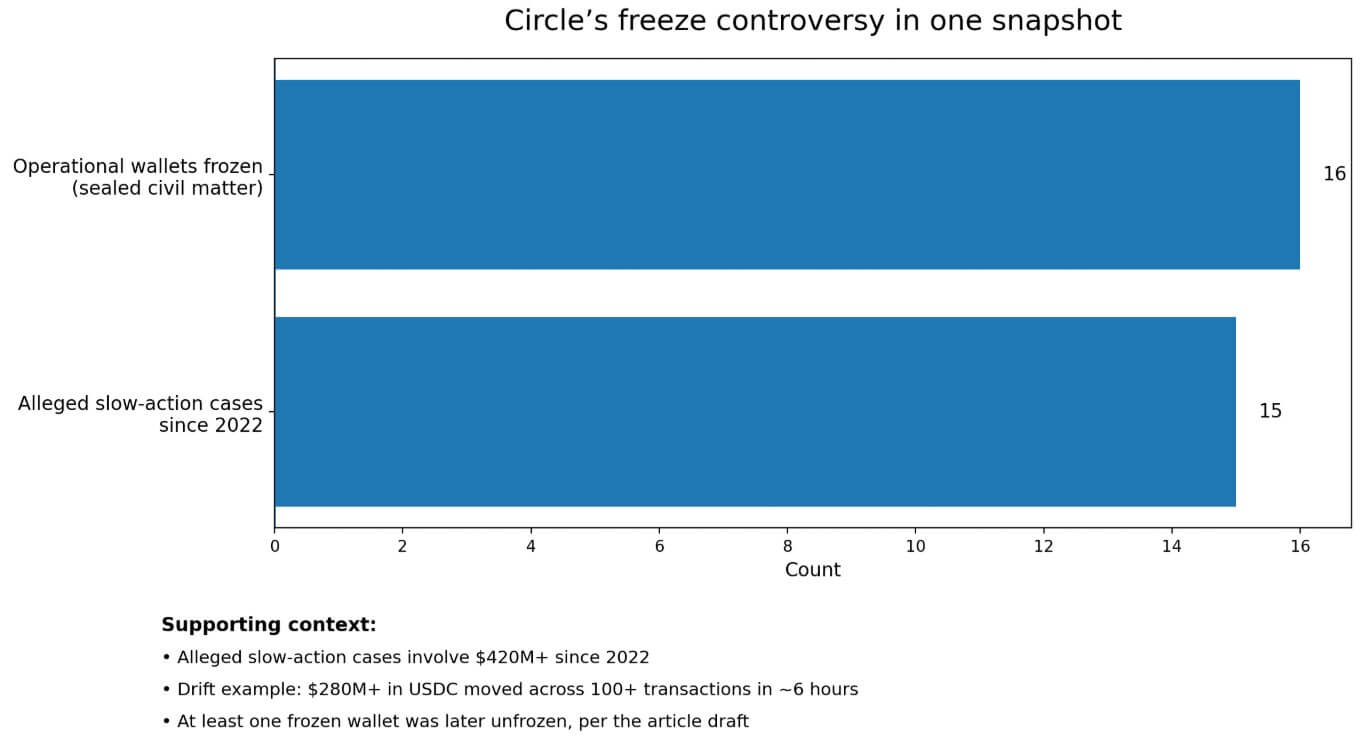

Circle was too slow in 15 cases involving more than $420 million in allegedly illicit funds since 2022, yet broad enough to sweep 16 operational business wallets in a sealed US civil matter. The wallets were tied to exchanges, casinos, and forex services that ZachXBT said did not appear connected.

Why this matters: USDC is a core settlement asset in crypto, widely used by exchanges, traders, payment flows, and DeFi protocols. Circle’s freeze decisions extend beyond individual legal disputes or hack responses and set the boundary for how much operational risk businesses accept when holding or moving dollars on-chain.

The firm later unfroze at least one of those wallets, belonging to Goated.com, adding weight to the question of how precisely Circle reviews the addresses it blocklists.

That sequence of “slow on theft, sweeping on civil process” lands at a difficult moment.

USDC held roughly $77.2 billion in circulation as of April 3, in a total stablecoin market of nearly $316.8 billion, accounting for about 24.5% of that pool. One of the cases ZachXBT cites, the Drift exploit, saw more than $280 million in USDC move across 100-plus transactions in roughly six hours.

At that scale and speed, the gap between “can freeze” and “froze in time” is the entire practical question.

The legal stack Circle built

Circle’s control surface has real on-chain teeth. Its EVM stablecoin contract includes a blocklist feature under a blocklister role, and blocklisted addresses cannot transfer or receive tokens.

Circle designed the contract to be both pausable and upgradeable.

That architecture existed long before this controversy arose, and Circle’s Access Denial Policy codifies when that power is triggered.

Circle can block individual addresses on every blockchain where its stablecoins are issued. Once denied, the associated balance cannot move on-chain.

The policy limits freezes to two narrow triggers: when Circle decides, in its sole discretion, that failing to act would threaten network security or integrity, or when a valid legal order from a recognized US or French authority requires it.

Reversals require formal confirmation that the legal obligation or security basis no longer applies.

The USDC Terms add a second layer. Nothing in those terms obligates Circle to track, verify, or determine the provenance of users’ USDC balances.

Yet, Circle also reserves the right to block addresses and freeze associated USDC that it determines, in its sole discretion, may be tied to illegal activity.

The Circle Mint User Agreement goes further: Circle may suspend accounts in its sole and absolute discretion, including under a court order, and may restrict redemptions or transfers when the law or a court order prohibits them.

The access-denial policy reads narrower and more formally rules-based, blocking sounds exceptional, tied to security events or legal compulsion. The broader USDC terms and user agreement grant the issuer considerably greater discretion.

Circle’s legal terms afford the issuer considerably more latitude than the access-denial policy’s narrow framing implies. When legal process and user continuity collide, Circle’s own hierarchy prioritizes compliance and issuer control.

| Document / layer | What it says Circle can do | Why it matters |

|---|---|---|

| EVM stablecoin contract | Blocklisted addresses cannot transfer or receive tokens; contract is pausable and upgradeable | Shows Circle’s control exists directly in token architecture |

| Access Denial Policy | Can block addresses across chains; freezes tied to network security/integrity or valid U.S./French legal orders | Frames freezing as narrow and exceptional |

| USDC Terms | Circle may block addresses and freeze USDC tied to suspected illegal activity in its discretion | Expands Circle’s room to act |

| USDC Terms | Circle is not obligated to track, verify, or determine provenance for users | Limits what users can expect Circle to do for them |

| Circle Mint User Agreement | Circle may suspend accounts in its sole and absolute discretion, including due to court orders | Shows compliance can override user continuity |

Where the criticism bites

The 16-wallet incident illustrates why that hierarchy now troubles operators. Circle’s freeze power executed quickly and broadly when a sealed civil matter arrived at its desk.

ZachXBT’s “Circle Files” allege the same power moved too slowly across 15 theft cases since 2022, and the Drift window, $280 million-plus across more than 100 transactions in six hours, is the sharpest example because the scale and transaction count appeared on-chain in real time.

The GENIUS Act, passed in July 2025, created a US regulatory framework for payment stablecoins, treating USDC-type products as regulated financial infrastructure.

The OCC’s implementing proposal has a comment deadline of May 1. FATF’s March 2026 report stressed that supervisors should assess whether blockchain analytics and controls deliver tangible enforcement outcomes, and that timely public-private coordination is crucial for asset recovery.

That is the precise standard ZachXBT and affected operators are now applying to Circle.

Circle markets USDC as fully backed, transparently managed, and the world’s largest regulated stablecoin. Circle’s own 2026 Internet Financial System report cited $50 trillion-plus in cumulative USDC settlement, 40% of stablecoin transaction volume, and 29% of stablecoin circulation as of September 2025.

At that scale, freeze governance operates at systemic weight, and the examination it now faces reflects the infrastructure role Circle has claimed for itself.

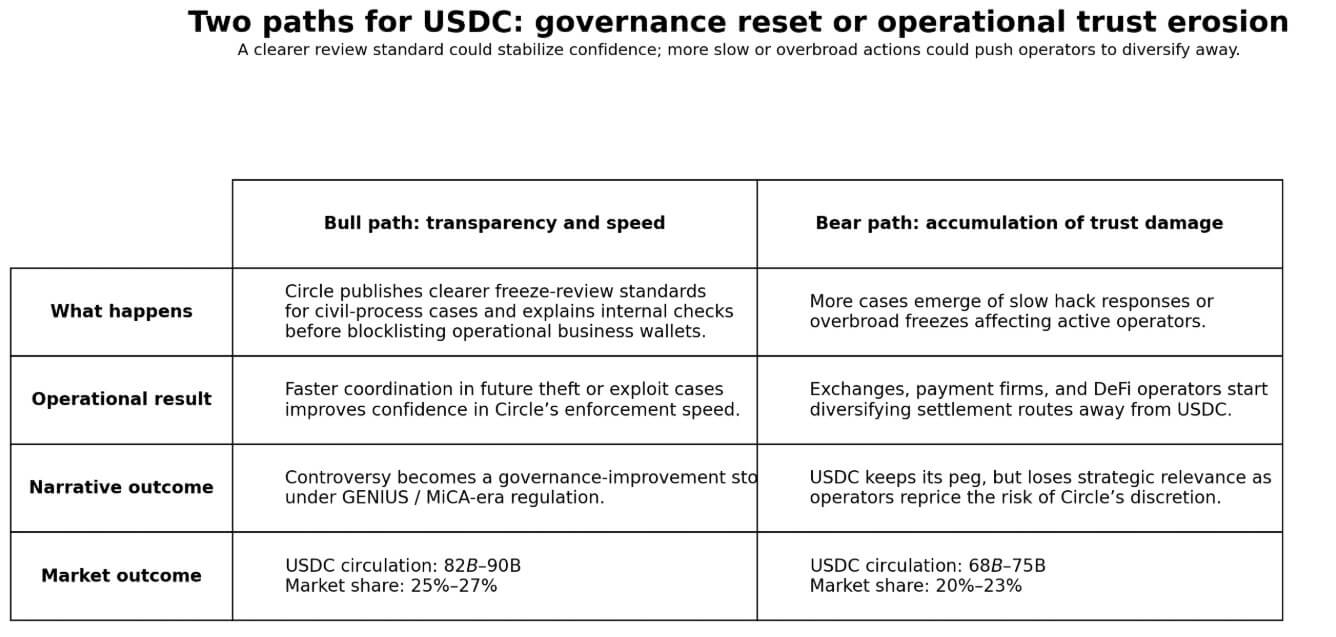

Two paths for Circle

The bull path runs through transparency and speed.

If Circle publishes a clearer review standard for freezes tied to civil process, detailing what internal review fires before Circle blocklists operational business wallets, and demonstrates materially faster coordination in future hack response situations, the controversy becomes a governance maturation story.

In that scenario, regulation under the GENIUS framework and MiCA rewards the most institutionalized issuer, and USDC circulation could recover to the $82 billion to $90 billion range, with 25% to 27% market share.

The 16-wallet incident, with Circle having already restored one wallet, would read as the moment Circle clarified its process.

The bear path runs through accumulation. More examples of slow hack responses or overbroad civil-process freezes, and operators who hold USDC in hot wallets, such as exchanges, payment companies, and DeFi protocols, are starting to diversify settlement routes.

A stablecoin can maintain its $1 peg while losing strategic relevance, and operators diversifying away from Circle would not trigger any depeg alert.

Tether, PYUSD, and a widening field of issuer-specific tokens each give operators a route away from Circle’s control stack.

In that outcome, USDC circulation drifts toward a $68 billion to $75 billion range and a 20% to 23% market share, as businesses reprice the operational risk of sitting within Circle’s discretion.

The next checkpoint arrives through operational performance, depending on how quickly Circle responds to the next hack, how quickly it restores blocklisted wallets, and if freezes land on operators with a clearer rationale than the last batch.

The OCC comment window closes on May 1, and the regulatory regime for payment stablecoins is taking shape while this dispute is live.

The market now wants to know if the compliance used by Circle model protects users or concentrates power in an issuer whose review standards operators cannot see.

Bitcoin

Bitcoin  Ethereum

Ethereum  Tether

Tether  BNB

BNB  XRP

XRP  USDC

USDC  Solana

Solana  Figure Heloc

Figure Heloc {kind=link}